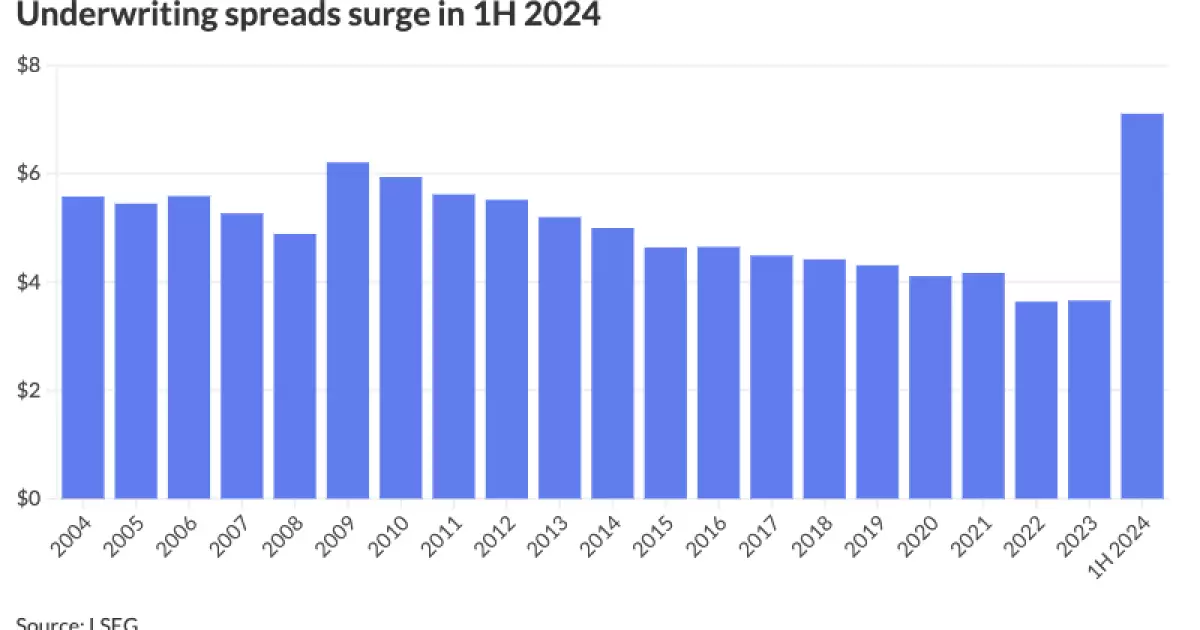

The first half of 2024 witnessed a significant surge in underwriting spreads for all types of bonds. The data reveals that underwriting spreads soared to $7.11 in the first half of 2024, marking the first time in 25 years that spreads have exceeded this threshold. This represents a substantial increase from the $3.70 recorded in the same period of the previous year, 2023. Moreover, the underwriting spreads for negotiated bonds rose to $6.55 in 1H 2024 from $3.78 in 1H 2023, while spreads on competitive deals experienced an even more dramatic uptick, increasing to $9.08 from $2.61 in the first half of 2023, according to data from LSEG. This escalation in underwriting spreads was observed across both refunding and new-money bonds, with the former climbing to $6.77 in 1H 2024 from $3.36 in the previous year, and the latter rising to $7.26 from $3.88 over the same period as reported by LSEG.

The gross underwriting spread represents the payment or discount that an underwriter receives for marketing a bond issuance. The current spike in underwriting spreads is primarily attributed to a variety of factors influencing the bond market dynamics. According to Wesly Pate, a senior portfolio manager at Income Research + Management, the scalability of underwriting costs plays a crucial role in this trend. If there is a disproportionate rise in the number of smaller deals in the market, it naturally leads to an increase in underwriting costs. This year, there has been a notable surge in the number of deals, surpassing the market value of issuance, which contributes to higher underwriting costs.

Matt Fabian, a partner at Municipal Market Analytics, suggests that the current market environment is characterized by high demand and limited space, resulting in a premium for primary market placements. Dealers are faced with more bonds in the market, which leads to a slower distribution process. The reliance on separately managed accounts (SMAs) further contributes to the delay in bond placements, as SMAs typically take longer to allocate bonds. In addition, the recent exits of major underwriters such as Citi and UBS from the market have reduced the level of competition among underwriters, subsequently driving up underwriting spreads.

Looking ahead, market analysts anticipate that the upward trend in underwriting spreads may persist in the second half of the year. The increase in issuance volume, coupled with uncertainties surrounding interest rates and bond prices, could further widen underwriting spreads. The potential outcome of the upcoming presidential and congressional elections also poses a risk, with the threat to the tax-exemption potentially leading to a surge in issuance and broader underwriting spreads. However, there are contrasting views regarding the longevity of this trend, as some experts believe that the current figures represent an outlier rather than a sustained pattern of higher underwriting spreads.

The escalation in underwriting spreads presents both challenges and opportunities for market participants. While the current economic environment and interest rate landscape may necessitate a higher margin of error for bond inventorying and ownership positions, the rise in underwriting spreads is seen as a welcome change that could provide a cushion against potential risks. As the bond market continues to evolve, stakeholders must closely monitor the impact of underwriting spreads on overall market dynamics and adapt their strategies accordingly to navigate the shifting landscape.