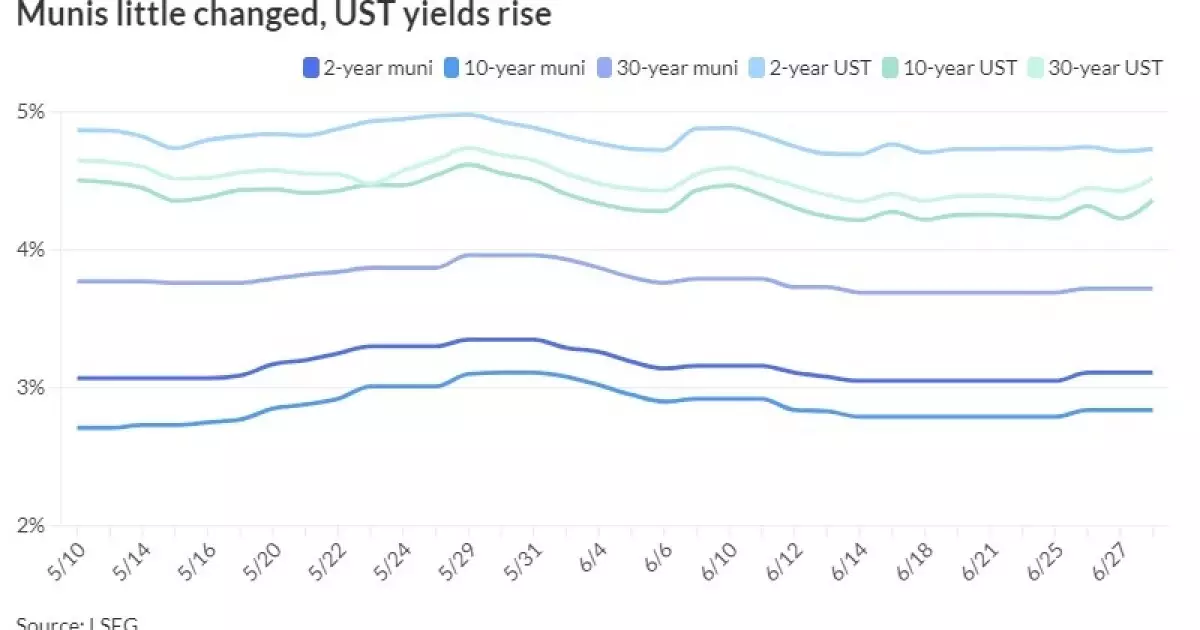

The month and the first half of 2024 for municipals came to a quiet end ahead of the Fourth of July holiday-shortened week. Despite a new-issue slate of only $240 million, there were significant movements in the market. Munis outperformed U.S. Treasuries on Friday, holding steady while govies saw some losses. Equities were also in the red following May’s personal consumption data. The market seemed largely unfazed by the first U.S. presidential debate, with analysts pointing towards gradual PCE inflation fall but still above the Fed’s 2% target. Overall, this quiet end to June sets the stage for potential shifts in the market dynamics going forward.

The Federal Reserve’s potential interest rate cuts have been a point of discussion in the market. Analysts like John Kerschner believe that the Fed now has the opportunity to consider a rate cut at their September 18 meeting. The anticipation of future rate cuts is tied to inflation data trends and the overall economic landscape. With two rounds of inflation data still to come before the meeting, market participants are closely watching for signals that could indicate a change in Fed policy. The U.S. electorate’s polarization and the recent presidential debate have added a layer of uncertainty to the discussion, as investors navigate potential impacts on their portfolios.

While the headlines have been dominated by political and economic events, the municipal bond market has been responding to other factors as well. U.S. Supreme Court decisions have had implications for the Securities and Exchange Commission and its enforcement mechanisms. The impact of these decisions on the public finance industry remains to be seen, but they could potentially shape how market participants operate in the near term. Market strategists have noted significant movements in Treasury yields, driven by heavy auctions and currency fluctuations. Despite these shifts, the muni market has shown resilience, successfully navigating a heavy primary market in June and maintaining relatively tight muni-to-Treasury ratios.

As July unfolds, market dynamics are expected to shift in favor of bond investors. With expectations of new long-term bond issuances and substantial principal redemptions, the market could see increased activity. Analysts at BofA anticipate a 100-basis-point rally in the second half of 2024, presenting opportunities for investors to enter positions. July’s issuance is expected to be in the mid $30 billion range, with the largest redemption month of the summer. Technical factors are likely to support the market, even with potential yield ascents and rate volatility. Despite this week’s selloff, Treasury yields have seen a slight decline in June, benefiting the muni market. High-grade bonds have outperformed, while other segments have faced challenges. Returns for different muni categories vary, with high-yield bonds showing strong performance in both June and 2024 so far.

The AAA yield curves across different indices have remained relatively stable, showcasing minimal changes in key maturities. Different market indicators, such as Refinitiv MMD, ICE, and S&P Global Market Intelligence, highlight consistent yields across various timeframes. The Bloomberg BVAL index also reflects steady yield levels across different maturities. Treasury yields have experienced fluctuations, with varying impacts on different securities. The overall market trends suggest a cautious yet dynamic environment for investors to navigate in the coming months.

The municipal bond market’s response to recent events and market trends indicates a complex landscape for investors. The interplay between economic indicators, Federal Reserve policy, political developments, and market dynamics creates both challenges and opportunities for market participants. Navigating these complexities requires a keen understanding of the factors at play and a proactive approach to investment strategies. As the market continues to evolve, staying informed and adaptable will be key to achieving success in municipal bond investments.