The summer of 2024 has proven to be more resilient for municipal bonds compared to the same period in 2023. According to AllianceBernstein strategists, the total returns for June through August last year were negative 0.04%, with August erasing the gains made in June and July as U.S. Treasury yields surged, causing muni yields to trend higher. Specifically, the 10-year muni bond saw a significant 36 basis point increase in August 2023. However, in contrast, this year’s returns for munis from June through August 16th are at a positive 3.11%, showcasing a stronger performance despite higher issuance levels.

Despite a surge in issuance levels, with issuers frontloading ahead of the upcoming November elections to avoid market volatility, the municipal bond market has shown remarkable resilience. Even with a slower pace of issuance on Thursday following a busy primary on Tuesday and Wednesday, major deals continued to be executed, such as the $1.8 billion worth of General Obligation bonds issued by New York City. Catherine Stienstra, the head of municipal bond investments at Columbia Threadneedle Investments, noted that despite the high levels of supply, the market has absorbed the issuance quite well. This can be attributed to the constructive nature of the muni market, driven by attractive yields that are higher than in the past, presenting an appealing opportunity for high-net-worth individuals to lock in these rates. Additionally, the influx of supply has not deterred separately managed account (SMA) growth, with SMAs absorbing a significant portion of the supply within 15 years, evident from the rich muni-UST ratios.

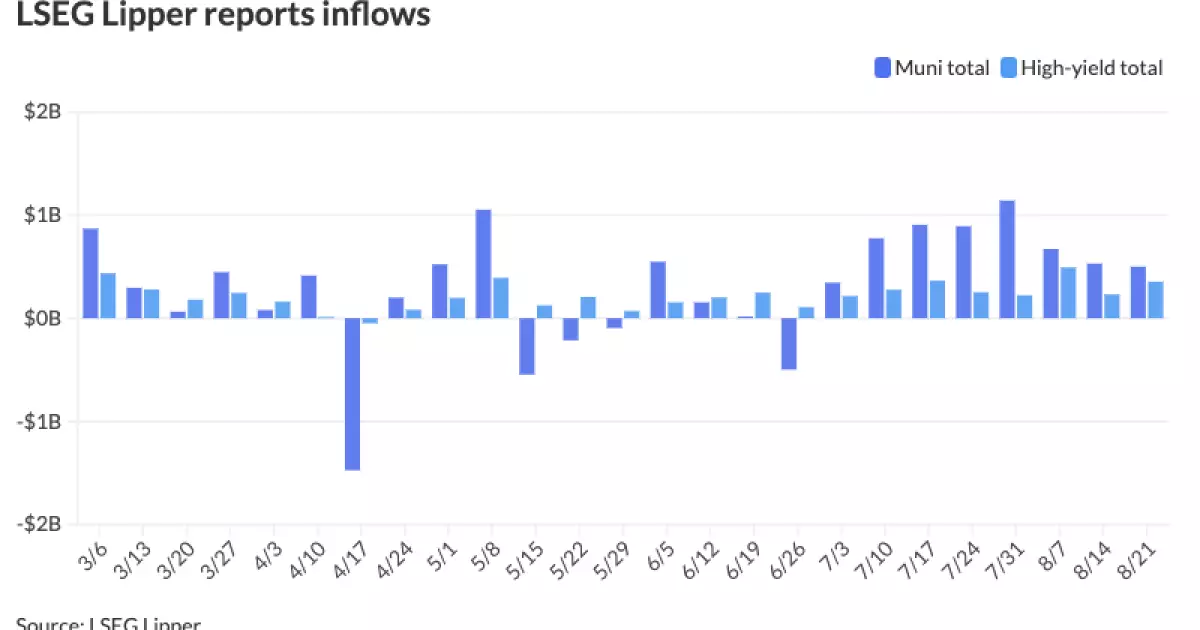

Despite the challenging market conditions and uncertainty surrounding Federal Reserve rate cuts, there has been a positive trend in fund flows into municipal bond mutual funds. Investors added $500.4 million to these funds after $530.3 million inflows the previous week, marking eight consecutive weeks of inflows. High-yield municipal bonds also demonstrated strength, with inflows of $354.8 million indicating investor confidence in the market. The upcoming Fed rate cut is expected to alleviate the volatility and duration concerns, potentially leading to increased inflows into the mutual fund sector.

The recent Federal Open Market Committee (FOMC) meeting minutes hinted at a possible rate cut by the Fed, with a majority of participants leaning towards a cut at the September meeting. However, the decision on the magnitude of the cut, whether 25bps or 50bps, still hinges on the next monthly employment report. Market analysts are closely monitoring the Fed’s stance, with expectations of a dovish emphasis from Fed Chair Powell’s upcoming Jackson Hole appearance. Any deviation from these expectations could lead to market disappointment, despite the anticipated rate cut in September.

In the primary market, several major issuances took place on Thursday, including bonds from cities like Dallas, Fort Worth, Los Angeles County, and Charlotte. These bond offerings indicate the continued demand for municipal debt instruments, with varying yields and maturities to cater to different investor preferences. Despite the prevailing market uncertainties, municipalities are leveraging the current market conditions to secure funding for various infrastructure projects and operational needs.

The municipal bond yield curve has remained relatively stable, with slight fluctuations in yields across different maturities. The AAA scales for various maturities reflect the consistency in yields, providing investors with transparency and pricing benchmarks. In comparison, U.S. Treasury yields showed a firmer trend, with an overall uptick in yields across different tenors. The movements in Treasury yields could impact the overall sentiment in the municipal bond market, as investors assess the relative attractiveness of munis versus Treasuries in the current interest rate environment.

The municipal bond market has demonstrated resilience in the face of market volatility, driven by strong investor demand, attractive yields, and strategic issuance planning by municipalities. Despite the uncertainties surrounding Fed rate cuts and economic indicators, the muni market continues to attract investors seeking stable returns and tax-exempt income opportunities. Moving forward, monitoring the Fed’s actions and market dynamics will be crucial for investors navigating the ever-evolving landscape of municipal bonds.