The municipal bond market has encountered a notable period marked by intricate dynamics amid a changing financial landscape. As various economic factors intertwine, understanding the subtleties of municipal trading, yield curves, and investment flows becomes imperative for stakeholders. This article explores the recent trends observed in the municipal bond market, particularly contrasting the performance of municipal securities against U.S. Treasury (UST) yields, the prevailing inflows and outflows in different investment vehicles, and the implications for investors going forward.

In the current analysis, the performance of municipal bonds has demonstrated resilience, especially when juxtaposed with the weaker performance within the U.S. Treasury market. The yield curves on triple-A rated municipal bonds remained largely stagnant, despite USTs registering losses of three to four basis points. Such inertia reflects a broader trend where municipal bonds have increasingly outperformed Treasuries this month. This growing preference for municipals can be attributed to their attractive yields and perceived safety amid market volatility.

The recent data illustrates that the ratios of municipal securities to USTs significantly dipped, with two-year municipals at 61% and 30-year bonds at 82%. This trend is indicative of heightened demand for municipals, which have been favored by investors seeking yield in a low-rate environment. Despite the availability of alternative options in the fixed-income market, investors continue to show strong interest in municipal bonds, highlighting the effective appeal of these securities in diversifying portfolios.

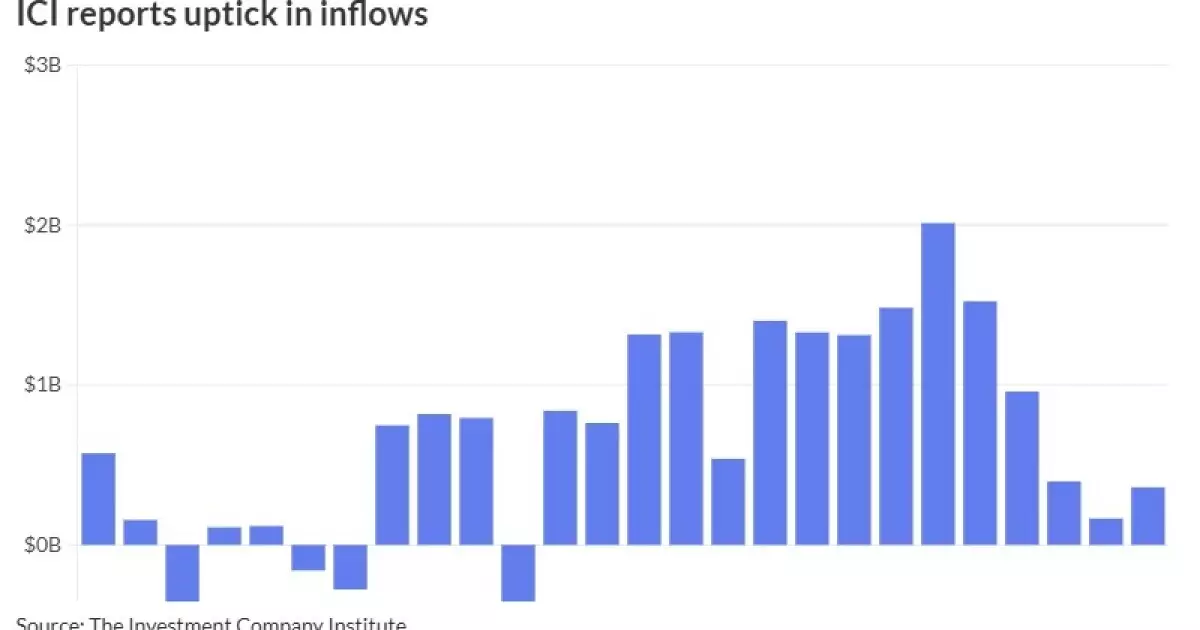

The Investment Company Institute reported a substantial influx into municipal bond mutual funds, totaling $360 million for the week ending November 13, marking an impressive streak of 14 consecutive weeks of inflows. This remarkable resilience contrasts sharply with the performance of exchange-traded funds (ETFs), which saw a significantly lower influx of $351 million. The divergence in inflows may reflect differing investor sentiments toward traditional mutual funds versus more volatile ETFs.

Amidst this backdrop, money market funds reported $88.2 million in outflows, indicating a cautious sentiment from investors within that segment. However, the yield for tax-free and municipal money-market funds has ticked up to 2.95%, signaling that while some investors are retreating, others are finding value in the income generated by municipal securities. The persistence of inflows into municipal bonds suggests an underlying confidence in their performance, even as other segments show signs of strain.

Interestingly, municipal bonds have shown positive yields, with investment-grade munis achieving a return of 0.81% for November and a year-to-date return of 1.63%. In contrast, USTs have struggled, posting a negative return of 0.40% for the month. This stark difference emphasizes how the municipal market is currently thriving amid a challenging economic environment. The appeal of municipals is further accentuated given their tax-exempt status, attracting investors (especially in higher tax brackets) looking for favorable after-tax returns.

High-yield sectors within the municipal market have also seen significant attention, with buyers continuously engaging through direct acquisitions and via mutual fund channels. The search for yield remains a key theme, driving the municipal segment to achieve strong gains over the year. The comparative attractiveness of bonds from issuers like Houston Airport underscores this trend, as the relative yields on comparable issues reflect the nuanced preferences among buyers.

Looking forward, the municipal market’s outlook remains cautiously optimistic, but challenges lurk. Macro-economic uncertainties, potential shifts in Federal Reserve policy, and evolving public finance needs can strain demand. The municipal market has benefited from favorable conditions, but any significant alterations in interest rates could unsettle its current equilibrium.

As seen in recent transactions, offerings are becoming more selective, affecting yields across different maturities. The near-term outlook for General Obligation (GO) sales, in particular, may be limited. This is vital to monitor, as it indicates potential shifts in investor appetite and subsequent pricing strategies for new issues.

While the municipal bond market has experienced a favorable scenario characterized by inflows and superior returns compared to USTs, it is crucial for investors to maintain vigilance. The interaction of market forces and economic indicators will shape future performance, and staying informed will be paramount for navigating the complexities of the municipal bond landscape.