October 2023 has concluded with a relatively stable yet unremarkable performance in the municipal bond market. While there was minimal movement in established bonds, the dynamics created waves across various sectors. Notably, although municipal mutual funds experienced overall inflows, high-yield segments witnessed their first outflows since mid-April, which raises questions about underlying investor sentiment. U.S. Treasuries displayed a mixed performance, and equities faced notable losses. The final session of October marked a notable point of reflection on the month’s overarching trends.

According to Kim Olsan, a senior fixed income portfolio manager at NewSquare Capital, the month experienced an upward trend in yield curves. The market correction offered a moment for buyers to seize attractive yields, showcasing how the economic landscape can shift what appears to be a momentary setback into an opportunity. The December finalization offers a chance to evaluate how this month’s correction could reshape investor strategies going forward.

The financial correction in October has not only translated into losses but has exposed significant vulnerabilities in bond performance. Data from Bloomberg indicates the Municipal Index registered a loss of -1.51%, the most significant decline since October 2009, which saw a drop of 2.09%. Comparatively, U.S. Treasuries recorded a more considerable loss of 2.42%, and corporate debts followed closely behind with a decline of 2.29%.

This sharp correction highlights the euphoria that often permeates market dialogues, which can swiftly turn to skepticism in tumultuous economic times. Olsan emphasizes the relative value focus among investors, noting that despite these losses, attractive yield ratios have spurred buyer interest. Wide ranges across different bond maturities continue to captivate attention, particularly in an environment where the demand for fixed investment products remains robust.

For example, the two-year municipal bonds are currently at a ratio of 65% against U.S. Treasuries, with similar metrics across durations. This dynamic not only underscores the attractiveness of municipal bonds but also signals potential shifts in investor strategy as they recalibrate for a more defensive positioning in response to market volatility.

In a compelling twist for investors, October has opened the door to substantial taxable equivalent yields. Olsan elaborates on how price fluctuations during the month have encouraged buyers to explore wider spreads while entrenching higher yield opportunities within reach. With one-year single-A rated revenue bonds trading at around 3.20%, this adjustment represents a favorable 30 basis points shift since September.

Olsan notes that AAA-rated bonds are breaking above a yield of 3%, with significant trades like Washington State’s 10-year GO bond yielding 3.24% which drives taxable equivalent yields to approximately 5.40%. Further along the maturity curve, investors are observing yields approaching 3.75% in AA-rated bonds, generating enticing opportunities for long-term investments.

This environment promotes defensive strategies that many investors would typically adopt during economic uncertainty. For instance, the pricing of New York City general obligation bonds at rates 30 basis points above prior trades reflects buyer willingness to engage in markets that they view as undervalued, ultimately leading to renewed interest in municipal debt.

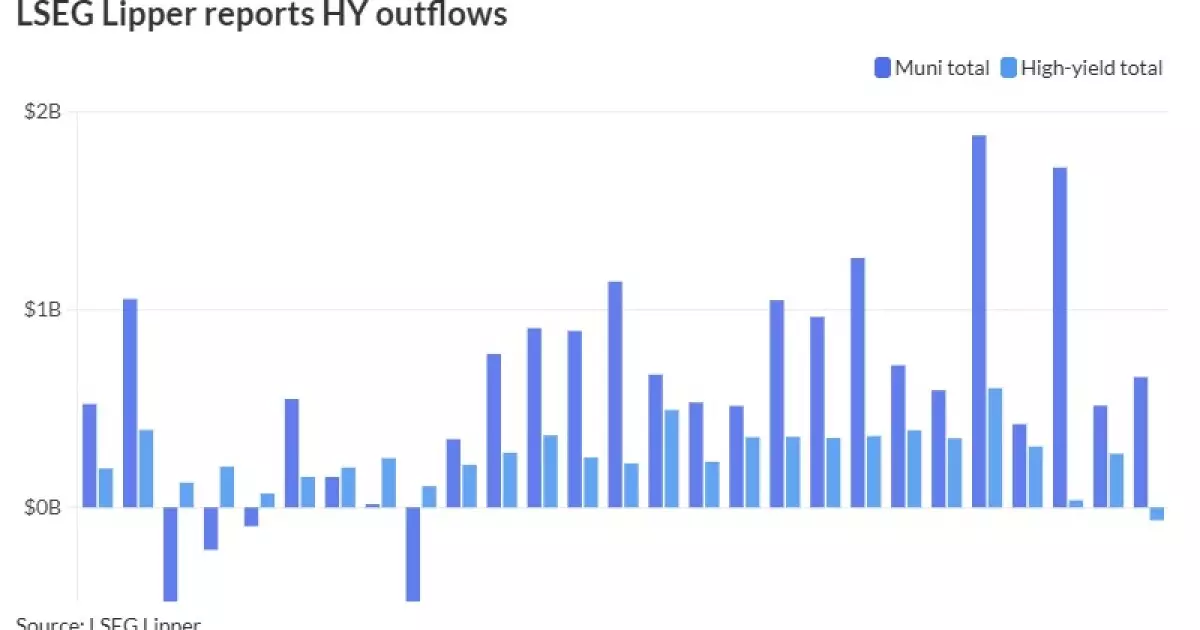

Even amidst current volatility, inflows into municipal bond funds remained robust as investors allocated $659 million during the last week of October—marking 19 consecutive weeks of positive inflows. This trend punctuates the resilience of municipal bonds as a defensive asset class amidst an environment littered with uncertainty.

Interestingly, high-yield funds saw an outflow of $64.4 million, contrasting sharply with the prior week’s inflows and potentially reflecting a cautious shift as investors pivoted towards more stable investments. Long-term funds captured a major share of this flow, and the preponderance of inflows through exchange-traded funds shows investors’ growing preference for liquidity amid fluctuating market conditions.

Money market funds also reported a noteworthy influx of $2.518 billion, showcasing investor confidence in immediate liquidity options, though yields on tax-free municipal money market funds saw a slight decline. The week-over-week changes remind market participants that even in periods of significant market movement, strategically positioned investments can yield substantial returns.

As the municipal bond market heads into November amid a backdrop of elections and economic transitions, expectations of continued volatility linger. However, newfound yield opportunities will likely attract a spectrum of investors seeking to capitalize on the month’s corrections.

The anticipated dip in issuance from the robust $56 billion in October could intensify demand, particularly when combined with underlying investor sentiment illustrated by recent fund flows. As market conditions evolve, positioning for the defensive while maintaining a diversified portfolio may become vital for navigating forthcoming uncertainties.

October 2023 has emerged as a critical turning point for municipal bonds and the broader financial market, propelling a narrative of both challenge and opportunity as investor strategies adapt to the landscape shaped by recent events.