The financial landscape for Build America Bonds (BABs) has experienced significant upheaval in 2024 due to fluctuating market conditions, increasing ratios, and a rise in interest rates. These factors have collectively contributed to a notable slowdown in BAB redemptions, even as some issuers express intentions to call back their bonds before the end of the year. Recent statistics from J.P. Morgan indicate that approximately $14.9 billion in BABs have already been called this year, with about $938.3 million scheduled for redemption shortly.

Despite some issuers moving forward with redemptions, broader market dynamics drastically influence their decisions. Issuers are expected to exercise the extraordinary redemption provision selectively, primarily when it is financially advantageous. With prevailing market conditions signaling higher rates—evidenced by the 10-year U.S. Treasury note reaching 4.27%—the feasibility of cost-efficient refunding diminishes. Nick Venditti, head of Municipal Fixed Income at Allspring, highlights that refunding BABs proves economically viable when rates are substantially lower than the current environment, a situation that is increasingly rare.

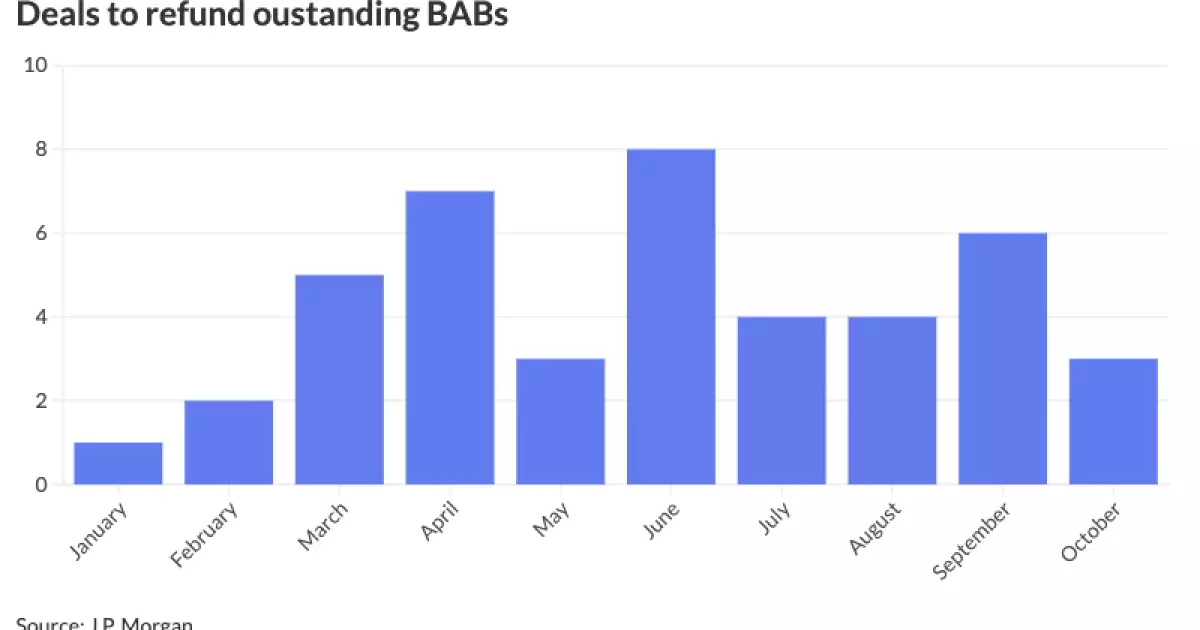

From a statistical perspective, the trajectory of BAB refundings has been uneven this year. The J.P. Morgan data reveals a slow commencement in the initial quarters, with a noticeable uptick in refundings during the second quarter, followed by a retreat in the third quarter. This irregularity may be directly tied to the rising interest rate environment, which has led to diminished enthusiasm among potential issuers looking to benefit from refunding opportunities.

The capture of market data presents intriguing patterns. A peak in the number of refunding transactions occurred in June, with eight deals hitting the market. April and October followed closely, each showcasing significant activity with seven and three deals, respectively. However, the earlier months of the year painted a vastly different scenario—January witnessed a singular deal, indicating a lack of confidence in the market amongst issuers.

A standout case of BAB refinancing this year emerged from the Los Angeles Unified School District, which executed a substantial $2.9 billion general obligation refunding bond in late April. This transaction underscored the potential for large entities to navigate the waters of rising interest rates; however, the caution adopted by other issuers reveals a more complex narrative. James Pruskowski, Chief Investment Officer at 16Rock Asset Management, notes a decline in BAB refinancings after the second quarter surge, attributing this trend to rising interest rates and a dampened urgency for refinancing.

Unpredictable market conditions have undeniably influenced issuers’ strategies. For example, the Ohio Water Development Authority recently postponed a scheduled refunding of $102.02 million in BABs due to adverse market volatility. The authority assessed that the potential net present value savings had been rendered minimal, prompting a halt in their transaction until conditions stabilize. This prudent decision reflects a broader caution among issuers, who are wary of the current economic climate’s impact on potential savings from refinancing.

Interestingly, the ripple effect of monetary policy changes, such as sequestration, plays a critical role in shaping issuers’ attitudes towards calling their BABs. The loss of the full interest rate payment subsidy forces many to reconsider their outstanding BABs, especially in light of the inherent call risk that discourages investor interest. Venditti articulates this sentiment, lamenting the current state of BABs as nearly uninvestable for many, as investors shy away from such bonds due to uncertainty surrounding their redemption.

As the year progresses, it becomes increasingly clear that the current uncertainty surrounding BABs has led to significant shifts in investor behavior. Municipal bonds, particularly taxable munis, have grown more appealing to institutional investors, including insurance companies that align assets and liabilities more strategically. Consequently, this diversion of attention away from BABs suggests a long-term trend driven by fiscal prudence and changing market appetites.

Teri Guarnaccia from Ballard Spahr notes a recent uptick in refunding deals despite the prevailing caution, indicating that some investors still see opportunity amidst adversity. Others, like Nixon Peabody, have experienced a marked decrease in inquiries about BAB refundings, indicating that while there is still interest in the asset class, it has been tempered by apprehension regarding redemption structures and market stability.

The landscape for Build America Bonds remains tenuous as factors contribute to a complex matrix of issuer and investor behavior. Moving forward, a careful balance between economic realities and strategic responses will dictate the trajectory of BAB refundings, shaping the market’s landscape for months to come. As volatility persists, it’s crucial for issuers to weigh their options and for investors to assess the inherent risks associated with BABs in this unpredictable market environment.