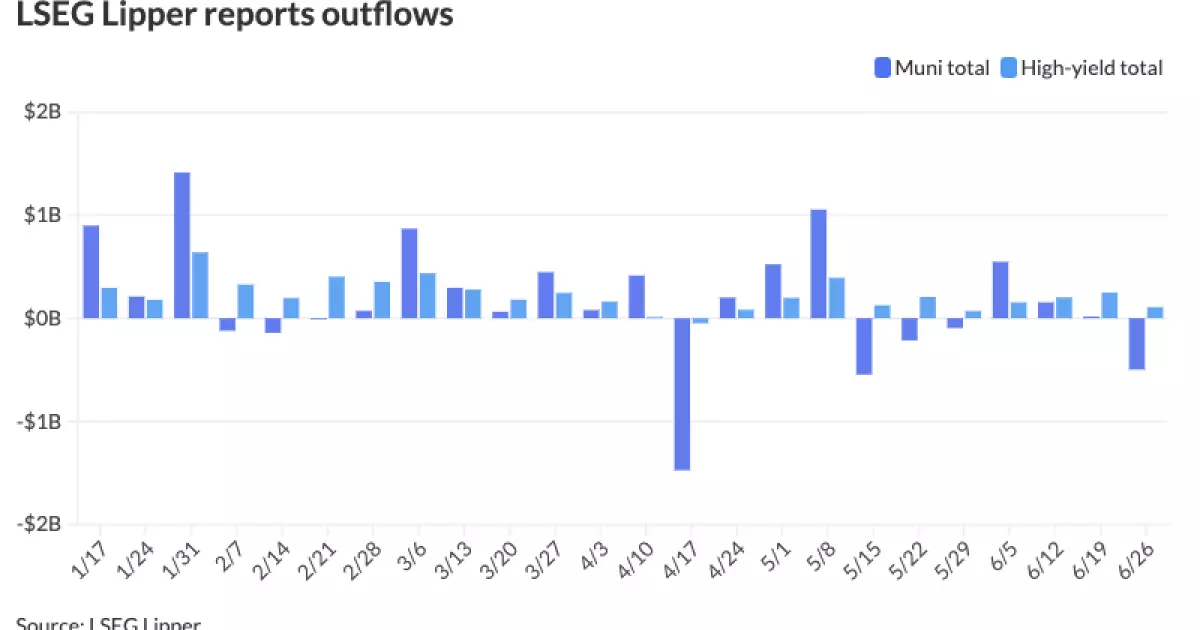

The municipal bonds market saw minimal changes on Thursday as the last of the largest deals priced. Although U.S. Treasury yields decreased and equities showed an upward trend towards the close of the day, municipal bond mutual funds experienced outflows. These outflows amounted to a significant $498 million, following an inflow of $16 million in the previous week. Notably, the two-year muni-to-Treasury ratio on Thursday stood at 66%, the three-year at 66%, the five-year at 67%, the 10-year at 66%, and the 30-year at 84%.

Investment demand in the municipal bonds market has been affected by several factors. With the Federal Open Market Committee meeting and the holiday-shortened week prior distorting market trends, it has become challenging to gauge a clear understanding of demand dynamics. This distortion has particularly influenced the rally in markets and the appetite for municipal bonds. Notably, the unusually structured $2.55 billion deal for the John F. Kennedy International Airport New Terminal One Project significantly bolstered demand, along with the high interest in AMT paper.

In the primary market, several key deals were priced by notable institutions. For instance, Morgan Stanley priced senior sales tax bonds for the Massachusetts Bay Transportation Authority, with significant cuts from the previous day’s pricing. Additionally, Jefferies priced revenue refunding bonds for the State Building Authority of Michigan, showcasing interest from investors in this security. The market also saw PSF-insured unlimited tax school building and refunding bonds priced for the Lewisville Independent School District and school improvement unlimited tax GOs for the Kings Local School District.

Looking ahead, the municipal bonds market is expected to witness a surge in new issuance, with a calendar of over $12 billion slated to close out June. However, the pace of new-money borrowings is projected to slow post the Fourth of July holiday, while the appetite for refundings may persist. Notably, reinvestment capital in July is anticipated to provide some relief to the market, especially during lighter holiday supply weeks. Additionally, the calendar for July and August is expected to see significant refunding capital, balancing the reinvestment capital during this period.

The yield curves for municipal bonds remained relatively stable with minor fluctuations in different maturities. Notably, the ICE AAA yield curve saw some cuts, while the S&P Global Market Intelligence municipal curve remained unchanged. Treasuries, on the other hand, exhibited firmer yields across various maturity points, reflecting the broader market conditions.

The municipal bonds market continues to show resilience amid changing market dynamics and investor sentiments. While challenges such as distorted demand trends and varying issuance volumes persist, the market’s ability to adapt and attract investors through structured deals and competitive pricing remains a key driver of growth and stability. Investors navigating this market should carefully assess the evolving landscape and capitalize on emerging opportunities for long-term value and returns.