The municipal bond market has recently witnessed notable enhancements, driven primarily by shifts in U.S. Treasury yields and fluctuating equity performances. As market participants navigate through a landscape shaped by recent Federal Reserve policies and economic uncertainties, key trends are emerging that bear implications for both investors and municipal issuers.

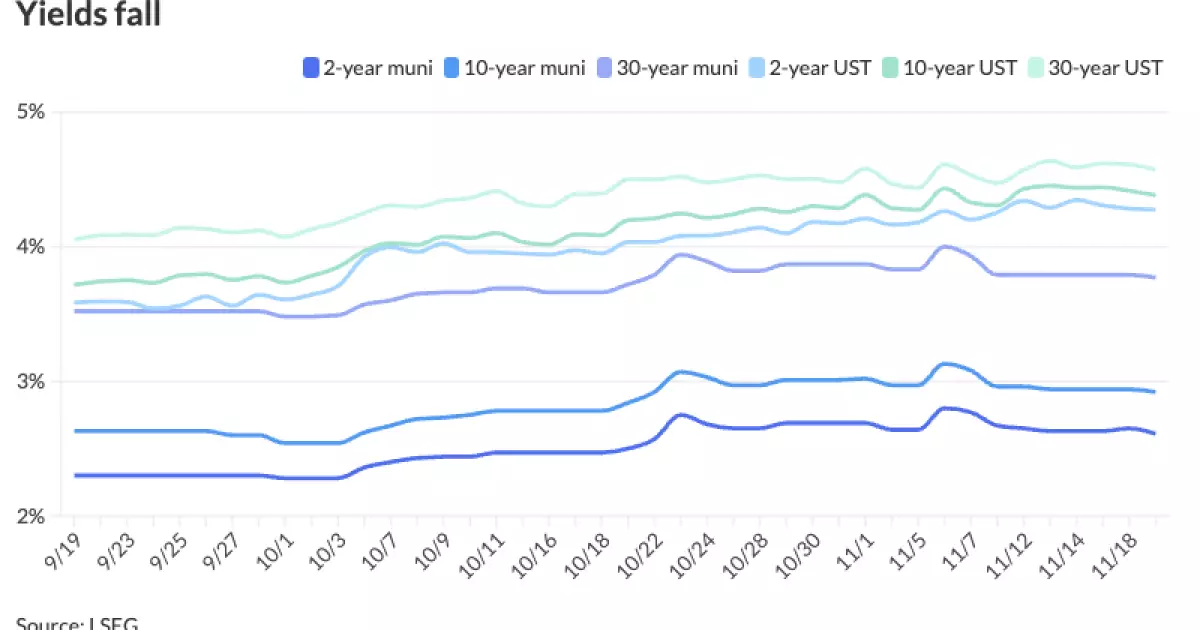

On a specified Tuesday, the municipal bond market displayed resilience, with the yields on Triple-A rated municipal bonds (munis) witnessing an uptick of one to six basis points across various maturities. In comparison, U.S. Treasury yields showed minimal improvement, particularly in longer maturities, indicating a complex interplay between risk, return, and investor sentiment. The compressed ratios, particularly in shorter maturities, underscore a growing preference for municipal bonds, which, despite current metrics suggesting that yields are on the low end of the spectrum, appear to attract robust demand.

Commentators, such as Chris Brigati, senior vice president at SWBC, have characterized the current supply conditions as markedly different from the pre-election period. The past month has observed a lighter issuance calendar, yet the upcoming weeks are anticipated to yield stronger municipal supply patterns. Significantly, the primary market still seems eager, bolstered by a notable $1 billion issuance from United Airlines for its Terminal project in Houston, highlighting solid investor interest in infrastructure and capital projects.

Retail investor behavior has been particularly noteworthy, with heightened enthusiasm for higher-income allocations driving a surge in smaller transactions. As Matt Fabian, a Municipal Market Analytics partner, notes, the demand for munis remains robust, with ratios falling to “uniformly rich levels.” This creates a compelling investment thesis despite the backdrop of rising yield expectations. The data reveals that shorter maturities – with the two-year muni to UST ratio at around 61% and the 30-year at an 82% ratio – signify a market where investors are increasingly valuing the fixed income stream of municipal bonds over that of Treasury instruments.

Adding a layer of complexity, mutual funds and exchange-traded funds (ETFs) are observing modest inflows, with separate managed accounts becoming a preferred channel for retail purchases. Total trade counts have risen again, reflecting the sustained interest in municipal issuances despite the broader market’s volatility.

As we approach the year-end, experts are pondering the potential trajectory of fund flows into municipal bonds. Notably, Fabian pointed out that the supply dynamics from the previous year saw significant inflows, and similar patterns might emerge this year, albeit with caution given the looming threat of tax reforms affecting the bond landscape. Current projections indicate that if the supply mirrors last year’s trends, it could lead to a total municipal supply nearing $500 billion by year’s end, which would be a significant milestone given the $451 billion already recorded.

With the environment continuously influenced by macroeconomic factors, including inflation and credit risk assessments primarily affecting Treasury securities, the outlook on yields remains bittersweet. Incremental price declines could be anticipated to sustain overall market fluidity, particularly if inflationary pressures compel the Federal Reserve to maintain or increase interest rates moving into 2024.

The primary market has seen various issuances making headlines recently. BofA Securities successfully priced nearly $1.1 billion in revenue bonds for United Airlines, illustrating demand resilience among larger institutional players. Other notable issuances include Goldman Sachs’s $782 million green bond for California Community Choice Financing Authority and a robust tranche from Connecticut’s Department of Transportation, which highlighted investor preference for secured debt instruments.

Furthermore, competitive bidding for other municipal projects underscores the vibrant market for revenue bonds, with various issuers ranging from transportation authorities to housing finance agencies seeking capital amidst favorable underwriting conditions. The competitive market’s response highlights the versatility of municipal bonds as a viable financial instrument for long-term planning and investment.

The municipal bond market’s current state is characterized by compelling yield opportunities, sustained demand from retail investors, and upcoming supply dynamics that may mirror historical patterns observed in recent years. Investors and issuers alike must remain vigilant, as ongoing economic developments will undoubtedly influence future performance and investment strategies. With distancing yet interconnected relationships between municipal bonds and U.S. Treasuries, the upcoming months will be crucial in determining the continued trajectory of this essential sector of the fixed income market.